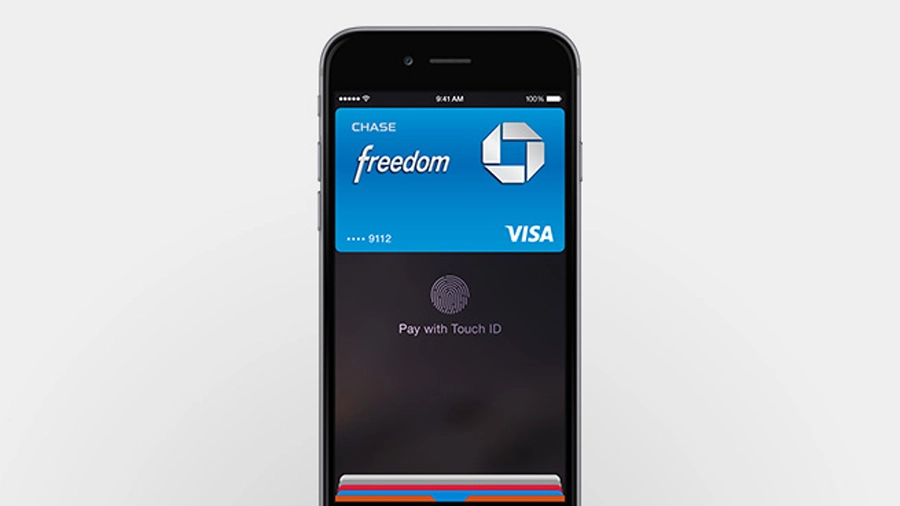

The Apple Pay function, tying Touch ID with mobile payments, was perhaps the most important announcement to come from the 9/9 event, and one that signifies the company's first legitimate claim to consumer identity.

The move pits Apple not just against payment providers such as PayPal, but against companies like Facebook, Google and Amazon as an identity provider.

Combining Apple Pay with Passbook effectively digitises a user's entire wallet, and with that their identity as a consumer. It's essentially putting your 'identity' into one 'pocketable' device.

This includes anything ranging from your credit or debit card, Tesco Clubcard, and student ID card, to your flight boarding pass, hotel room key, and restaurant voucher. Developments in the world of the Internet of Things will even enable you to unlock your car via NFC-enabled devices in the not-so-distant future – you can already do it with your home.

- Check out everything businesses need to know about Apple Pay on our sister website, ITProPortal.com

While other identity providers have offered businesses a way to get users to register and log into their sites for years, Apple has the scale to compete as a major player in consumer identity from the outset. What's more, it will be joining the party armed with millions of iPhone users and over 200 million credit cards on file.

NFC payments have so far failed to take off, but Apple Pay is likely to turn the tables on a so-far sluggish take-up. A number of other companies have tried to apply the technology to payments before and have failed because they couldn't make the user experience seamless enough, regardless of merchant adoption. What's significant about Apple Pay, however, is that Apple may have found the mobile payments holy grail by tying identity, credit cards, Touch ID, and NFC together.

Interface and user experience will be crucial for wide adoption by consumers, but if there's one company that understands how to do this, it's Apple. With its huge customer base, and backing from major US banks, retailers and online companies that are already planning to accept Apple Pay, Apple is perhaps the only company that can make NFC payments useful and popular.

Apple is not alone in recognising the importance of payments in the race to own consumer identity however. Facebook, for example, which allows for social login – a feature that permits users to sign into their favourite websites using their social media profiles rather than entering their personal data – applied to the European Union earlier this year for a license for money transfer capabilities. This is part of what is believed to be Facebook's plan to incorporate payments into its messaging platforms. Facebook also owns WhatsApp, which has a huge international subscriber base – especially in the developing world.

Whilst Apple is yet to confirm whether or not it will take a commission or charge a fee for its role in the payment process; even with an intermediary charge it is not expected to generate substantial profit from the new feature. Instead, Apple Pay will seek to draw users further into the Apple eco-system. Apple Pay, combined with Passbooks and HomeKit really will make your iPhone 6 the key to your digital life.

- Patrick Salyer is the CEO of Gigya, a consumer identity management platform.